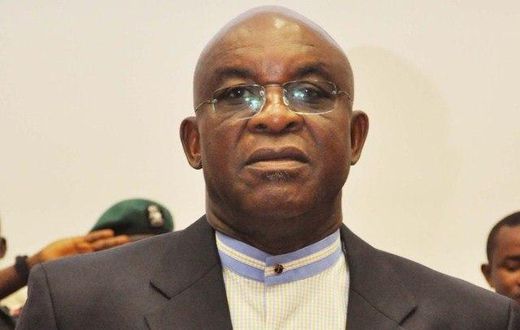

Ghana’s Minister-designate for Finance, Dr. Cassiel Ato Forson, has underscored his determination to eliminate the Electronic Transactions Levy (E-Levy) and other so-called nuisance taxes, in accordance with President John Mahama’s campaign promise to deliver sweeping reforms within 120 days of taking office. This pledge has sparked conversations not only in Ghana but also among financial observers and businesses across West Africa, including Nigeria, where digital transaction taxes have been actively debated.

Dr. Forson has asserted that the E-Levy poses a significant threat to Ghana’s journey toward a cashless society. First introduced in 2022, the E-Levy applied a 1.5% charge to all electronic transfers that exceeded GH₵100 per day. Despite the government’s subsequent move to reduce the rate to 1%, the measure has continued to attract criticism from various segments of society—business leaders, consumer advocates, and economists—who argue that the tax is regressive, hampers economic inclusion, and ultimately places a disproportionate burden on ordinary citizens.

While Nigeria does not currently have a direct equivalent to Ghana’s E-Levy, discussion around the taxation of digital financial services—combined with the country’s vibrant fintech ecosystem—means that Ghanaians’ experience is being closely watched by Nigerian policy makers, business owners, and everyday users of mobile money and banking applications. According to Lagos-based economist, Ifeanyi Mbanefo, “The implications of Ghana’s policy experiment have been instructive for Nigeria, particularly as we try to encourage digital payment adoption while safeguarding government revenue.”

During his vetting session before Ghana’s parliament on Monday, 13 January 2024, Dr. Forson reiterated his unwavering standpoint about the levy. He stressed that, should he assume the ministerial position, the E-Levy would be scrapped at the very first budget session of a new administration. According to Forson:

The E-Levy is neither a direct tax, indirect tax, nor an excise tax. I don’t know how to classify the E-Levy as a tax practitioner. Mr Chairman, it doesn’t mean I don’t recognise that the E-Levy brings in certain revenue. But the fact remains that the E-Levy retards our progress toward a cash-light economy and fintech. We need to abolish the E-Levy.

E-levy

He went on to elaborate:

I am on record saying that, given the opportunity to abolish the E-Levy, I would. I want to restate that position. If approved, as part of the first budget, I will announce that we will abolish the E-Levy. His Excellency President Mahama committed to this in our 120-day agenda, and we stand by it.

To address anticipated shortfalls in government revenue, Dr. Forson revealed that the planned abolition will be matched with deliberate spending cuts. He explained that rigorous expenditure control would fill any financial gap that may result from the loss of E-Levy collections. As he noted:

It shouldn’t always be about revenue, revenue, revenue. Why not pay attention to expenditure? Remove the E-Levy, don’t replace it, and cut corresponding expenditure.

The E-Levy was introduced by the Government of Ghana as a way to shore up public finances after the COVID-19 pandemic and global financial shocks put unprecedented pressure on revenue sources. According to the Ghana Revenue Authority, officials had originally projected the E-Levy would generate up to 6.5 billion Ghanaian cedis (about ₦466 billion or US$530 million) in 2022 alone. However, actual collections fell short of these ambitious targets, raising questions about the effectiveness and fairness of the policy.

The levy has also been deeply unpopular with digital entrepreneurs and small businesses, who fear that it discourages everyday transactions, stifles innovation in the mobile money sector, and undermines customer trust. In focus group discussions held by the Ghana Chamber of Commerce, many traders have reportedly reduced their reliance on electronic payments and returned to cash transactions, partly to avoid additional levies. This sentiment resonates with small business owners in Nigeria, who have in recent years voiced concerns over rising bank transfer fees and other transaction charges.

In West Africa, digital payments have seen explosive growth over the past decade. The West African Monetary Institute estimates that platforms such as mobile money, agency banking, and cardless transfers now process trillions of naira worth of transactions annually, transforming the speed and convenience of shopping, money transfers, and bill payments. However, the debate over how best to tax this growing sector remains unresolved. Ghana’s E-Levy ordeal has become a cautionary tale for other African regulators: how do you balance the government’s need for revenue with the broader goal of financial inclusion and digital transformation?

According to research from Nigeria Inter-Bank Settlement System Plc (NIBSS), Nigeria’s digital transaction volume rose by over 50% year-on-year in 2023, with mobile and online banking driving much of the growth. Experts warn, however, that aggressive taxation or poorly designed levies could drive people back to informal cash systems or trigger the rise of underground remittance networks—risks that Ghana’s experience brings into sharp relief for policymakers in Abuja and across the region.

The Nigerian context further complicates the discussion. While Nigeria’s Central Bank at times has sought to encourage digital adoption (such as reducing USSD fees and collaborating with fintech startups), it has also implemented currency redesign and cash withdrawal policies that many consumers view as deterrents to seamless digital payments. Against this backdrop, Ghana’s bold promise to eliminate the E-Levy—despite government revenue challenges—has been widely discussed in the Nigerian business press and among tech influencers.

Notably, some analysts warn that the absence of transaction taxes could leave a gaping revenue hole. “Ghana’s challenge highlights the broader dilemma facing African governments: public services need funding, but excessive fiscal pressure can damage innovation and exclude the most vulnerable,” notes Abimbola Adebayo, a Lagos-based policy consultant, in a recent interview. For citizens in both countries, the real question is whether governments can find fair, sustainable, and pro-business ways to expand their tax base without undermining the drive toward cashless and inclusive digital economies.

The fate of Ghana’s E-Levy will serve as an important lesson for Nigeria and similar emerging markets. As Dr. Forson’s team prepares its budget plans and lawmakers in Accra weigh the next steps, stakeholders across West Africa will be following closely to see whether the abolition of digital transaction levies can promote broader digital adoption, stimulate local businesses, and help achieve long-standing developmental goals.

How should African governments fund public services while supporting digital financial innovation? Should Nigeria, Ghana, and other countries invest more in broadening the tax net rather than targeting transactions that drive inclusion and economic activity?

Share your opinions in the comments below and follow us for more in-depth analysis on African business, policy, and technology trends.

Want general support, or have questions about submitting your story? Reach out at [email protected].

Join our community for the latest updates—follow us on

Facebook,

X (Twitter), and

Instagram.

Connect, share, and let’s keep the conversation going on the business of Africa!